Batteries are “hot commodities” It takes time to scale up a project, yet battery raw materials prices have soared sharply since the beginning of 2021, leading to speculation that either demand destruction or hold-ups would affect demand as well as the perception that automotive manufacturers could change their taste over electric vehicles.

Battery Chemistries and the EV Industry

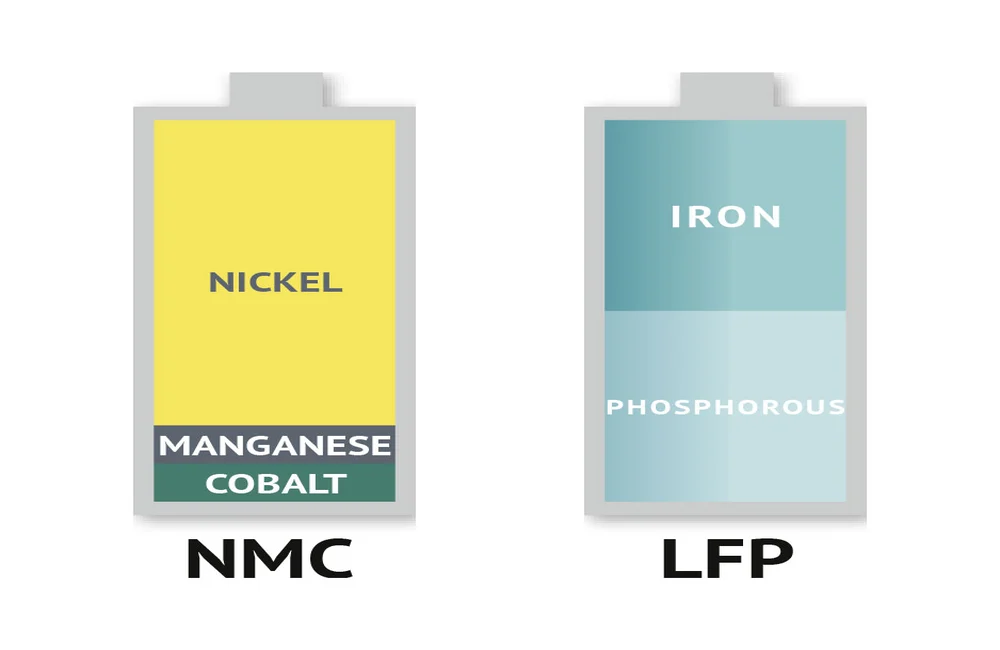

The cheapest pack has always been lithium-iron-phosphate, or LFP. Tesla has already been using LFP in entry-level models built in China since 2021. Other automakers like Volkswagen and Rivian have also said they would use LFP in their most affordable models.

Nickel-cobalt-manganese, or NCM, batteries are another choice. They need about as much lithium as LFP, but they also have cobalt, which is both pricey and the subject of some controversy in its supply chain.

Cobalt and Nickel Prices

Cobalt metal price is up 70% on the year. Nickel has faced fresh drama after a short squeeze on the LME. On May 10, the three-month nickel price is trading at $27,920–$28,580/mt in the intra-day range.

At the same time, in 2021, the prices for lithium skyrocketed by over 700%, causing a huge spike in battery pack pricing.

Chinese battery metal costs were 580.7% higher year on year in March for LFP batteries on a dollar per kilogram basis, according to S&P Global Market Intelligence, with costs reaching nearly $36/kWh. NCM batteries rose 152.6% YoY in February to $73–78/kWh.

"We made a note that the way lithium has been priced up of late, it is a smaller discount than what you would expect [against NCM], and when you start throwing on performance factor, it is a tougher decision than it would have once been. You may want to sacrifice some performance for cost, but it isn’t much cheaper these days,” said one cobalt hydroxide seller.

“There were concerns, for sure, given the price of LFP was climbing too much for the market that it serves, which is budget batteries,” a source within a lithium producer agreed.

“There are no established alternatives to nickel-intensive batteries (batteries that contain 8 parts nickel or more) near- or mid-term. A return to lower-nickel NMC batteries brings back the cobalt question, while LFP batteries can’t yet fully compete with range capabilities and have a relatively poor low-temperature performance compared with nickel-rich batteries,” said Alice Yu, senior analyst, S&P Global Market Intelligence.

Dominance of LFP and NCM in Markets

The current dominant chemistry in China is the LFP battery, but NCM is generally expected to represent a much larger role in the EU markets, where customers prefer cars that will take them across their country or continents in as few charges as they can manage.

“When we think about designing battery plants, we think about flexibility. At present, there is cost equivalency between LFP and NCM. If LFP is much cheaper again, we can get them to work with them, but to be honest, at the moment we should produce NCM because it is a premium product," said an automotive OEM.

Another auto OEM reiterated the comment: "LFP batteries will be there for entry-level vehicles, but not adopted for premium cars."

Limiting Factor: Lithium Supply

Lithium supply is still a huge worry for the EV market, and an obstacle that could prevent any company from easily transitioning to LFP.

Propensity also seems to come from research from S&P Global Commodity Insights, which finds that even if every lithium mine currently in the pipeline starts production in the proposed timeframe and with the right specs for battery-grade material, the shortfall will still be 220,000 mt by 2030 if demand reaches 2 million mt by the end of the decade.

Western lithium producers have their largest share of output sold under long-term contracts, while Chinese converters have been active on both the spot and long-term contract fronts. “There are some [spot] requests, but we have no material available," a lithium producer source said. “We have volumes only when a customer has some issue or cancels a shipment for some reason, otherwise, all is booked,” he added.

"Fears over lithium and other battery metals becoming the bottleneck in enabling EV uptake have led automakers to get more involved with the upstream side of the industry in recent years." Controlled Thermal Resources' Hell's Kitchen lithium project in California will receive a boost from General Motors investment. Stellantis, Volkswagen, and Renault teamed up with Vulcan Resources to source material from the No Carbon project in Germany.

Sodium-Ion Batteries: A Potential Alternative

Supply of these metals is expected to be short in the next few years. Due to this, the battery industry is running both heartily and testing out alternatives. One of those will be sodium-ion batteries.

Sodium-ion will generally use carbon in the anode and materials from a class of compounds known as Prussian Blue in the cathode. "There are a series of metals which can be used on Prussian Blue, and it will vary depending on the company," says Venkat Srinivasan, the director of the US-based Argonne Collaborative Center for Energy Storage Science (ACCESS).

The biggest advantage for sodium-ion is its cheaper production cost, said the sources. Because sodium is so plentiful on earth, these battery packs could almost be 30–50% cheaper than lithium-ion batteries. The energy density is in the same ballpark as LFP.

Last year, one of China’s largest battery manufacturers, Contemporary Amperex Technology (CATL), presented its first-generation sodium-ion battery, as well as its AB battery pack solution that demonstrated CATL’s capability of incorporating sodium-ion cells and lithium-ion cells into one pack. The sodium-ion battery is also compatible with existing lithium-ion battery manufacturing processes and equipment, according to CATL.

But some concerns need to be addressed before sodium-ion can get to a meaningful commercial scale.

Optimizing the electrolyte and the anode sides is still possible. Compared to a standard LFP-based battery, sodium-ion has a strong discharging, but comparatively weak charging.

The principal limiting factor is that this is still a few timeframes away from being at a commercial capacity. Likewise, billions of dollars of investments have already been placed in the lithium-ion supply chain based on lithium- and nickel-rich chemistries.

“Sodium-ion absolutely would be a contender, but we need to first address what's out there and bringing the plant online,” one battery maker said.